Wasp Barcode Technologies: The Barcode Solution People

From the Experts: Secrets for Cash Flow Success

It’s what determines a company’s strong or weak image, the financial position your company is in and it even determines business failure and success. This influential force is cash flow.

What exactly is cash flow? To put it simply, it’s the total amount of money being transferred into and out of a business, especially as affecting liquidity. Managing cash flow remains one of the top accounting problems reported by small business owners. 51% of small business owners cite cash flow as their ‘biggest challenge’. Concerns related to a weak cash flow are often expressed with terms like “flat sales” or “margins are off,” but whatever terms are used, business owners are asking one question: where has their cash gone? “A fairly large percentage of small businesses end up in some sort of crisis over cash in the first couple of years of their existence,” says Dave Kurrasch, a former senior vice president at Wells Fargo and current vice president and general manager of Small Business Payments Company. “That’s why the fatality rate in small business is so high.”

Companies showing “anemic gross profits and slow turnovers,” writes James McNeill Stancill, a professor of finance at the University of Southern California, in a Harvard Business Reviewarticle find that their growth lags, often leading to a higher need for external financing. On the other hand, companies with a strong cash flow are able to invest and generate more cash, resulting in higher growth.

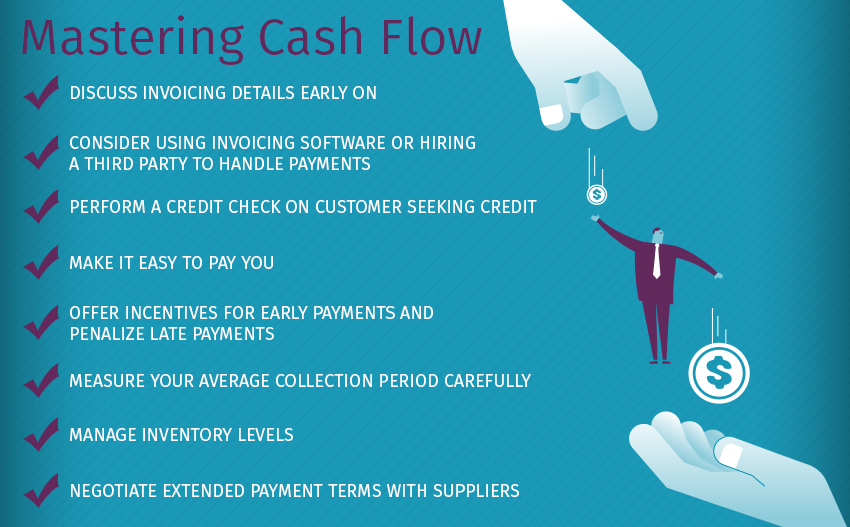

So, how can small businesses take charge of their finances? Below are three important components to improve cash flow:

Discuss invoicing details early on

Keep a tight handle on accounts receivables

What is accounts receivable and how does it affect your cash flow? According to BizFilings’ the definition, accounts receivables “represent sales that have not yet been collected in the form of cash.” For example, “an account receivable is created when you sell something to a customer in return for his or her promise to pay at a later date.”

An alarming 80% of small business owners receive late payments for their services, according to a 2011 survey by PaySimple. When this happens, it negatively affects cash flow, impacts inventory and operating expenses.

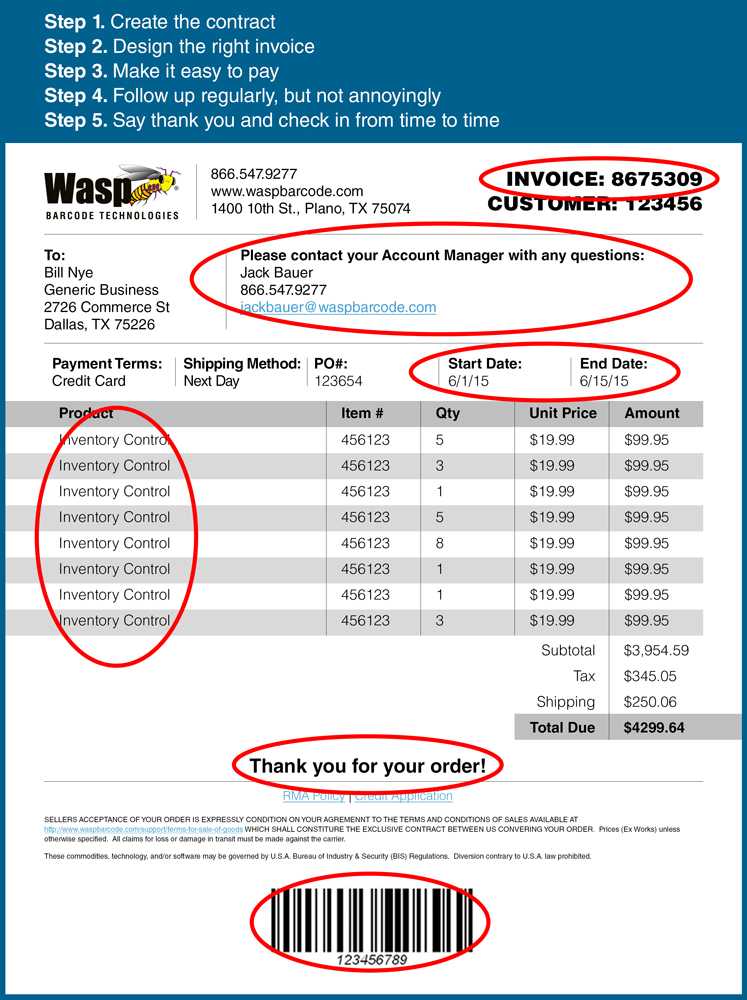

[caption id="attachment_8247" align="alignleft" width="235"] Tips for Invoicing - Click to expand[/caption]

In short, accounts receivables are investments that you make to your customer. The longer your customer takes to pay on their accounts, the longer money is tied up in your own accounts and the more negatively your cash flow is impacted. When customers don’t pay in a timely manner, it creates cash shortages, especially if you’re a small business owner who needs the money to pay your bills or invest in other obligations to expand your business. The situation gets more complicated when you factor in components such as credit terms, which is the time limit you set for your customers to pay, and credit policy, which are the factors you consider when extending credit to a customer. If your business is the kind that typically extends credit to its customers, then accounts receivables is something you need to constantly keep a close eye on.

To prevent your accounts receivables from negatively affecting your cash inflows and outflows, consider the tips below for invoicing and getting paid:

Don’t leave any chances for delays to occur when it comes to invoicing. From the start, you should find out how each client prefers to receive their invoices. Ask what kind of information you need to provide, how you should invoice, when you should invoice, and who you should send your invoices to. In an article on the U.S. Small Business Administration, Caron Beesley advises to state your payments term clearly in your invoice. For example, include a specific term such as “Payment due in 30 days” rather than “Due upon receipt,” which is vague.

“If you are an independent contractor, state clearly who the payment should be made to, especially if you operate under a ‘Doing Business As’ or trade name, but retain a bank account in your own name, you want to ensure the check is written to you,” says Beesley.

Consider using invoicing software or hiring a third party to handle payments

Business owners have a lot of responsibilities, so no matter how diligent, it’s inevitable that you’ll lose track of an invoice here or there. Using invoicing software or hiring a third party to stay on top of this financial responsibility for you can fix this problem, keep you organized, and help get your invoices out more promptly. Many programs keep track of how long it takes a customer to pay you, when invoices are past due, and when they need to be submitted.

When it comes to improving your accounts receivable practices and efficiency, there are no shortages of tools to choose from. In his Forbesarticle, Gene Marks, CPA and owner of The Marks Group, lists a few technologies that can help manage your accounts, including:

When it comes to improving your accounts receivable practices and efficiency, there are no shortages of tools to choose from.

KnowledgeSync is software that connects with most accounting databases and notifies users when there are “overdue receivables, shortages of inventory, quotes that aren’t followed up timely or orders that miss deadlines.” (Price: Under $5,000)

Anytime Collect is a financial management application that focuses solely on accounts receivable invoicing information, “sending out collection letters and emails to overdue customers (and supporting multiple contacts at an account), tracking activities (such as calls and emails) made with customers, maintaining notes, reporting on collection activities, recording cash payments” and filing it all in an easy-to-understand format.

Bill.com is basically an outsourced accounts payable department where you send your invoices to them and they take care of “scheduling, approval, notifications, payments (printed checks or electronic) and then syncing back to your accounting system.” (Price: $19 to $50 per month per user)

Perform a credit check on customers seeking credit

The Fair Credit Reporting Act allows you to buy a credit report on customers seeking credit from your business, which can help reduce any unknown issues that can later affect your cash flow. While these reports are preemptive, they have the potential of disqualifying good candidates, warns an article on the Small Business Chronicle.

Make it easy to pay you

From checks to debit cards to online processing services like PayPal, Stripe, Braintree, and Authorize.Net, make paying you simple and easy for all your customers. If most of your customers use PayPal, you should still consider the small percentage of customers who don’t. How will you make it easy for them to pay you?

An article in Small Business Trends points out a few questions you should ask yourself when it comes to choosing the right payment methods:

Do you want to accept payments by phone or on your mobile device in person?

Do you only want to accept standard credit card payments (Visa, Mastercard, Discover, AMEX, etc.) or do you also want to accept newer payment methods like Apple Pay, Bitcoin, or Venmo?

Do you need subscription billing? Split payment options?

Do you have customers worldwide and in countries that can’t use PayPal?

Offer incentives for early payments and penalize late payments

One business savvy way to get customers to pay you on time is to get them to pay you early. Many will happily agree to do so if they get a chance to save in the end. An Intuit article discusses this strategy: “A five or ten percent discount for early payments provides a real incentive for customers to open their wallets sooner. Make sure the discount is advertised obviously on the invoices you send out, and make sure you can afford to offer the money off, too.”

On the other hand, charging a fee or interest on late payments is the best way to get customers to stop sending their payments in late. Moreover, you have the legal right to do so.

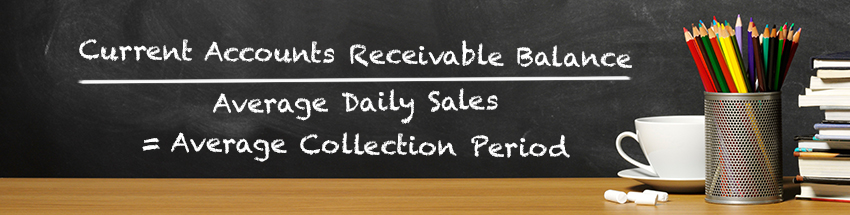

Measure your average collection period carefully

How long should you give customers to pay you? This period should be carefully considered since it “defines the relationship between accounts receivable and your cash flow,” says BizFilings.

“A longer average collection period requires a higher investment in accounts receivable. A higher investment in accounts receivable means less cash is available to cover cash outflows, such as paying bills.”

According to BizFilings, the average collection period is calculated by dividing present accounts receivable balance by average daily sales (average daily sales amount divided by 360. If you use the previous quarter’s sales instead of annual information, divide the sales amount by 90 instead). See below:

Manage Inventory Levels

Properly managing inventory is crucial to all businesses and failing to do so is one of the major reasons small businesses fail, according to the U.S. Small Business Administration. Yet, 46% of small businesses (11 to 499 employees) don’t currently track inventory or use a manual process. As a result, business owners can easily lose track of inventory and negatively affect their cash flow. In these instances, companies endure steep costs comparable to “burning money,” as Marcus Lemonis assured on his CNBC show The Profit.

Inventory is defined as any “extra merchandise or supplies your business keeps on hand to meet the demands of customers.” Carrying an excess amount of inventory can “dramatically decrease your cash flow,” says Chris Garner, accounting manager at Informatics, and advises that “it’s important that a business tracks inventory turns, and sets an appropriate metrics for their business model.” On the other hand, running out of stock can cause you to lose customers and risk your company’s reputation along the way.

According to “accounting coach” Harold Averkamp, CPA and MBA, an increase in inventory indicates that you have purchased more goods than you can sell.

Up as a negative number on your cash flow statement because it affects the cash you have on hand. He writes: “Negative amounts on the statement of cash flows can be interpreted to mean 1) a cash outflow, 2) that cash was used, or 3) that it was unfavorable for the company's cash balance. In other words, you can think of negative amounts as having a negative effect on the company's cash balance.”

Forward-thinking companies know that they need to carefully keep a handle on inventory to maximize sales and maximize costs, which would yield to higher overall profits. With properly implement inventory management, businesses can increase their turnover to 4.5 times per year.

A post in SageWorks explains how you can properly manage inventory:

“One way to better manage cash flow is to forecast sales as accurately as possible. This can be done by looking at previous sales over the last 12 months and finding sales trends month-by-month. Another option is to use a just-in-time inventory (JIT) management system.”

“Make sure your inventory practices are more ‘just in time’ than “just in case”,’ said John Blasingame

“Make sure your inventory practices are more ‘just in time’ than “just in case”,’ said John Blasingame, Florence, Ala.-based President of Small Business Network and host of the Small Business Advocate radio show. The main idea behind JIT inventory management is to procure inventory right before it’s needed. This will reduce inventory holding costs and create more free cash flows.”

Negotiate extended payment terms with suppliers

In very much the same way that late payments from customers negatively affects your cash flow, so does paying your vendors in measurements that don’t benefit your business’ bottom line.

This area of accounting is called accounts payable and is defined as the “amounts you owe to your suppliers that are payable sometime within the near future, ‘near’ meaning 30 to 90 days.”

For optimum cash flow management, carefully consider your payment schedule and negotiate a term that benefits both you and your vendor. For example, think about what you can offer to get a longer payment term, perhaps getting on a 60-or 90-day schedule instead of a 30-day one. If this frees up the cash you need to grow sales, make it known to your supplier that you’ll increase your order if they allow you longer periods for payment. This is similar to a short-term loan in that it enables you to hold on to the cash you need.

However, while there are many benefits to longer payment terms, be cautious of the disadvantages that these terms can cause.

“While slow paying your vendors may be tempting, your suppliers are one of your most valuable partners,” says Marks. “Be careful not to be a notorious slow paying customer, because you may suddenly need something from them in a pinch. In these days of low interest rates it makes more financial sense, not to mention business sense, to pay your bills early and take a discount if offered."

As a small business owner with multiple responsibilities, accounting might be the last thing you think about. The longer you put off components that affect a healthy cash flow, the more money you’re at risk of losing. When the cash you have on hand is razor-thin, it’s vital that you’re accurate at forecasting cash flow. To do this, you need to monitor the above components, which are extremely imperative to the financial health of your company.

How could these tips help your business cash flow?

This site uses cookies. By closing this banner, scrolling this page, clicking a link or continuing to browse, you agree to the use of cookies. If you want to know more about how we use cookies on this site, please review our Privacy and Cookie Policy. To review Wasp's GDPR Policy, click here.

It’s what determines a company’s strong or weak image, the financial position your company is in and it even determines business failure and success. This influential force is cash flow.

What exactly is cash flow? To put it simply, it’s the total amount of money being transferred into and out of a business, especially as affecting liquidity. Managing cash flow remains one of the

It’s what determines a company’s strong or weak image, the financial position your company is in and it even determines business failure and success. This influential force is cash flow.

What exactly is cash flow? To put it simply, it’s the total amount of money being transferred into and out of a business, especially as affecting liquidity. Managing cash flow remains one of the

According to “accounting coach” Harold Averkamp, CPA and MBA, an increase in inventory indicates that you have purchased more goods than you can sell.

Up as a negative number on your cash flow statement because it affects the cash you have on hand. He writes: “Negative amounts on the

According to “accounting coach” Harold Averkamp, CPA and MBA, an increase in inventory indicates that you have purchased more goods than you can sell.

Up as a negative number on your cash flow statement because it affects the cash you have on hand. He writes: “Negative amounts on the